Are you a business owner in Bangladesh looking to navigate the complex world of VAT registration? Understanding the ins and outs of Value Added Tax (VAT) is essential for all businesses operating in the country. In this blog post, we will unlock the secrets of VAT registration & Turnover Enlistment in Bangladesh, breaking down the process step by step to help you easily navigate this important aspect of running a business. We will provide you with practical tips and insights to simplify the VAT registration & Turnover Enlistment and ensure compliance with the law. Stay tuned to gain a deeper understanding of VAT registration in Bangladesh and take your business to the next level.

Why is VAT Registration Important for Businesses in Bangladesh?

VAT Registration is crucial for businesses in Bangladesh because it is mandatory for entities with annual turnover exceeding the threshold set by the government. It enables businesses to legally collect and remit VAT on their sales, ensuring compliance with tax regulations.

What is Turnover as per VAT Act 2012 ?

“Turnover” means, in relation to a person, all the money received or receivable by such person within a prescribed time or tax period against the supply of taxable goods or the rendering of taxable services, manufactured, imported or purchased by means of his economic activities; [Section 2(42)]

What is Registration Threshold & Enlistment Threshold as per VAT Act 2012 ?

“Registration Threshold” means the limit of Taka 3 (three) crore as turnover of an economic activity of any person in a 12 (twelve) month-period, but does not include the following, namely-

(a) the value of an exempted supply;

(b) the value of sale of a capital asset;

(c) the value of a sale of an organization of economic activities or any portion thereof;

(d) the value of a supply made as a consequence of permanently closing down an economic activity; [Section 2(57)]

“Enlistment Threshold” means the limit of Taka 50 (fifty) lac as turnover of an economic activity of any person in a 12 (twelve) month- period, but does not include the following, namely-

(a) the value of an exempted supply;

(b) the value of sale of a capital asset;

(c) the value of a sale of an organization of economic activities or any portion thereof; or

(d) the value of a supply made as a consequence of permanently closing down an economic activity; [Section 2(48)]

When registrations are required for the purposes of VAT?

(1) Each of the following persons shall, from the first day of a month, be required to be registered for VAT, namely—

- a person whose turnover exceeds the registration threshold (i.e. Tk. 3 crore) within a 12 (twelve)- month-period closing at the end of the month preceding that month; or

- a person whose estimated turnover exceeds the registration threshold (i.e. Tk. 3 crore) within the succeeding 12 (twelve)- month-period beginning at the start of the preceding month. [Section 4]

Example:

1. Assume that today is 29 July 2024. FM Ltd prepared its financial statements for year ended 30 June 2024 and reported sales revenue is Tk. 30,800,000

Answer: FM Ltd. has recorded actual sales totaling TK. 30,800,000, surpassing the threshold of Tk. 3 crore. Therefore, VAT registration is mandatory for FM Ltd.

2. Assume that today is 20 July 2024. FM Fashion Ltd prepared its financial statements for the month of June 2024 and reported sales of Tk. 2,600,000. However, the company is expecting its average revenue per month will be Tk. 2,900,000 for next 11 month.

Answer: FM Fashion Ltd. is projected to achieve sales of (2,900,000 x 11) = Tk. 31,900,000, exceeding the threshold for VAT registration, which is required to obtain VAT registration.

When is VAT registration mandatory?

Every person carrying on the following economic activities must be registered for VAT regardless of the turnover threshold, if he—

(a) supply or manufacture or import goods or services which are subject to supplementary duty (SD) in Bangladesh;

(b) supply goods or service or both against any contract or work order or through participating in the tender;

(c) Involved in any export and import business.

(d) Establish branch office or liaison office or project office of a foreign organization.

(e) Appointed as VAT agent.

(f) Engaged in economic activities related to supplies, manufactures or imports of specific goods or services or in any specific area as determined by the National Board of Revenue (NBR). [Section 4]

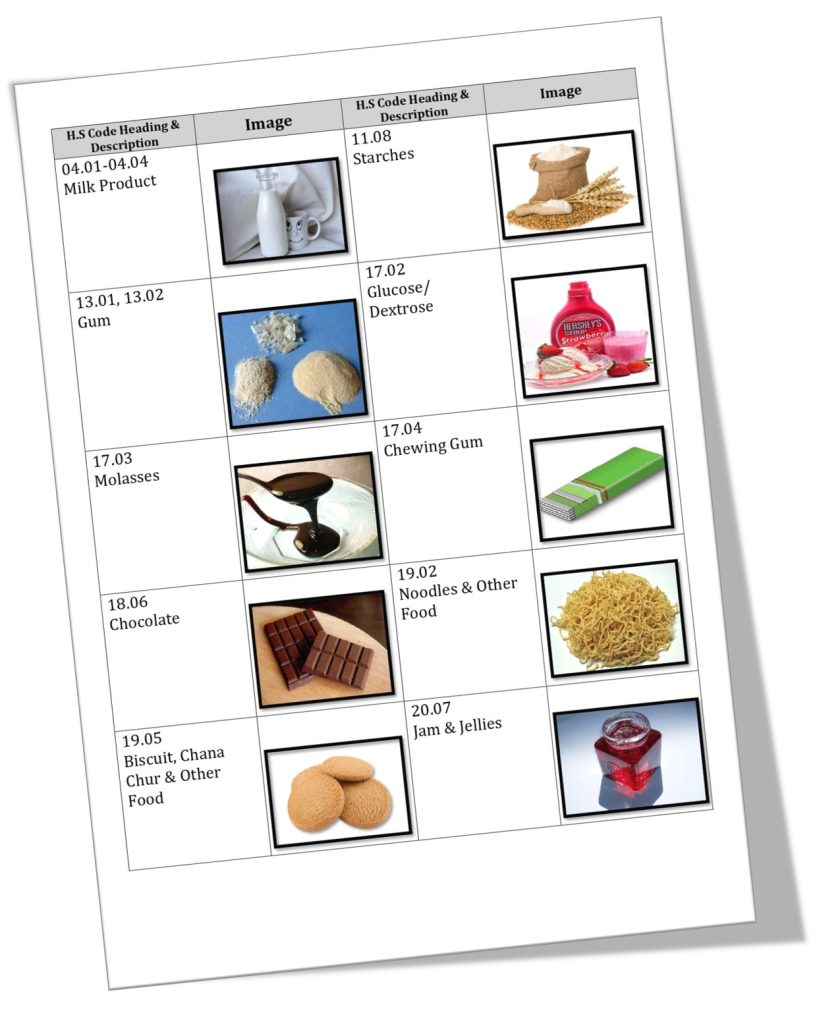

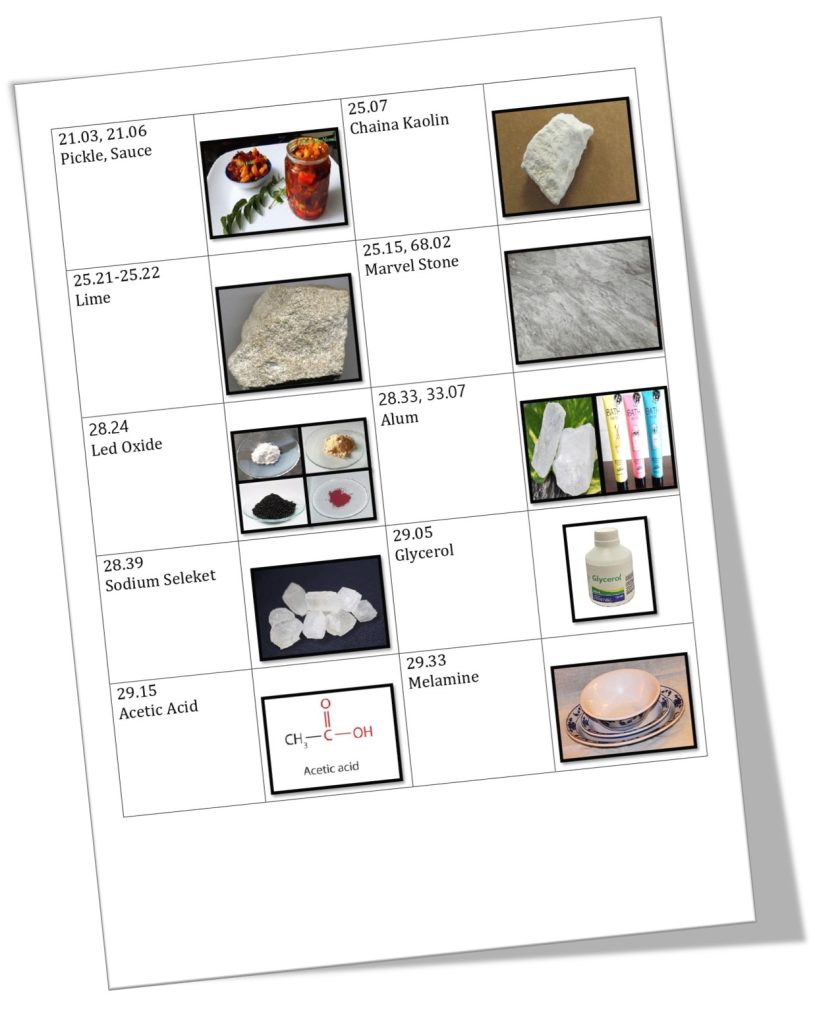

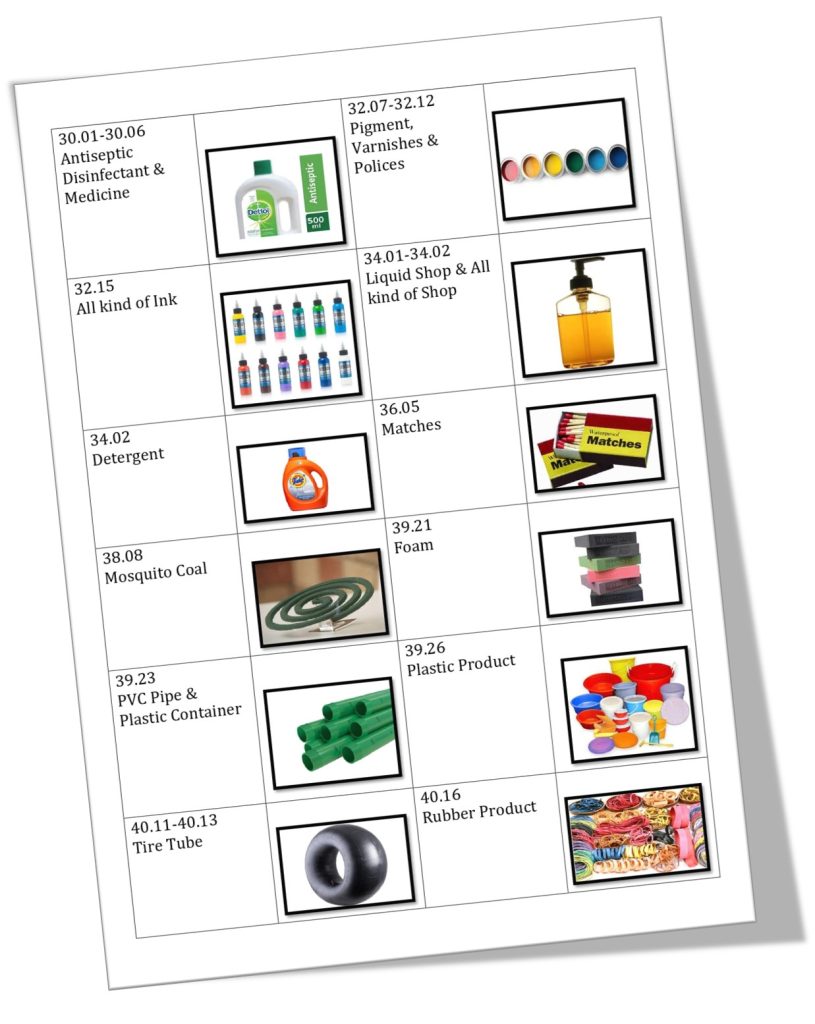

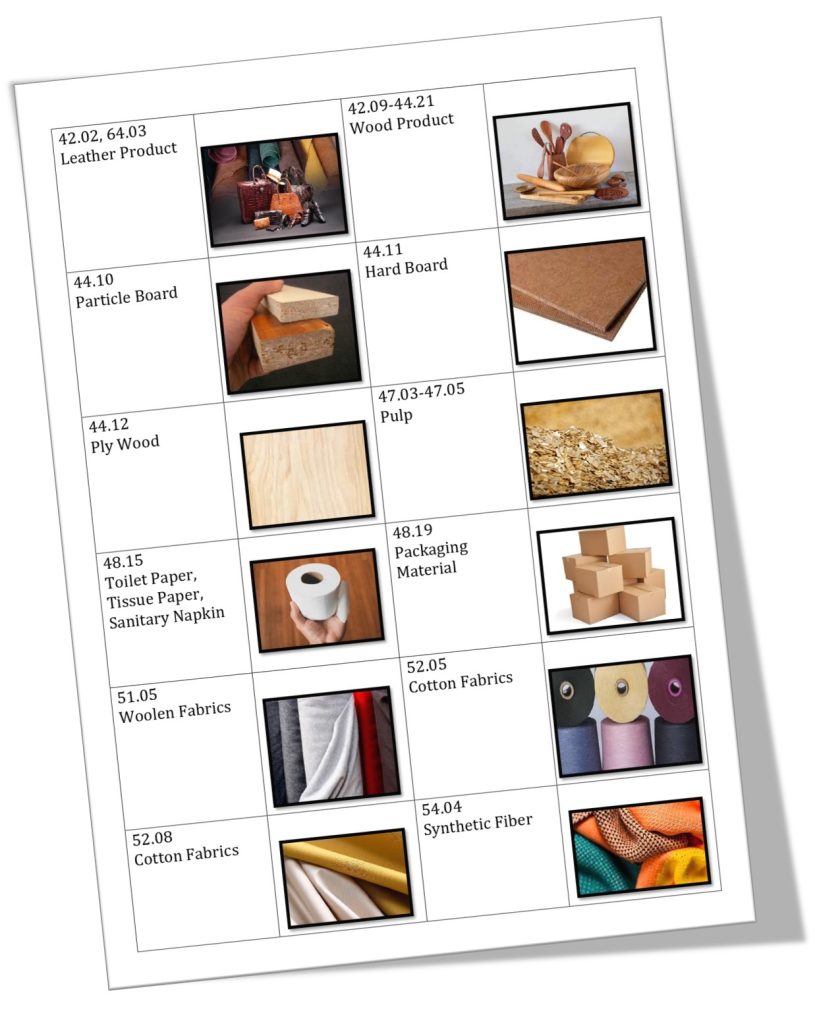

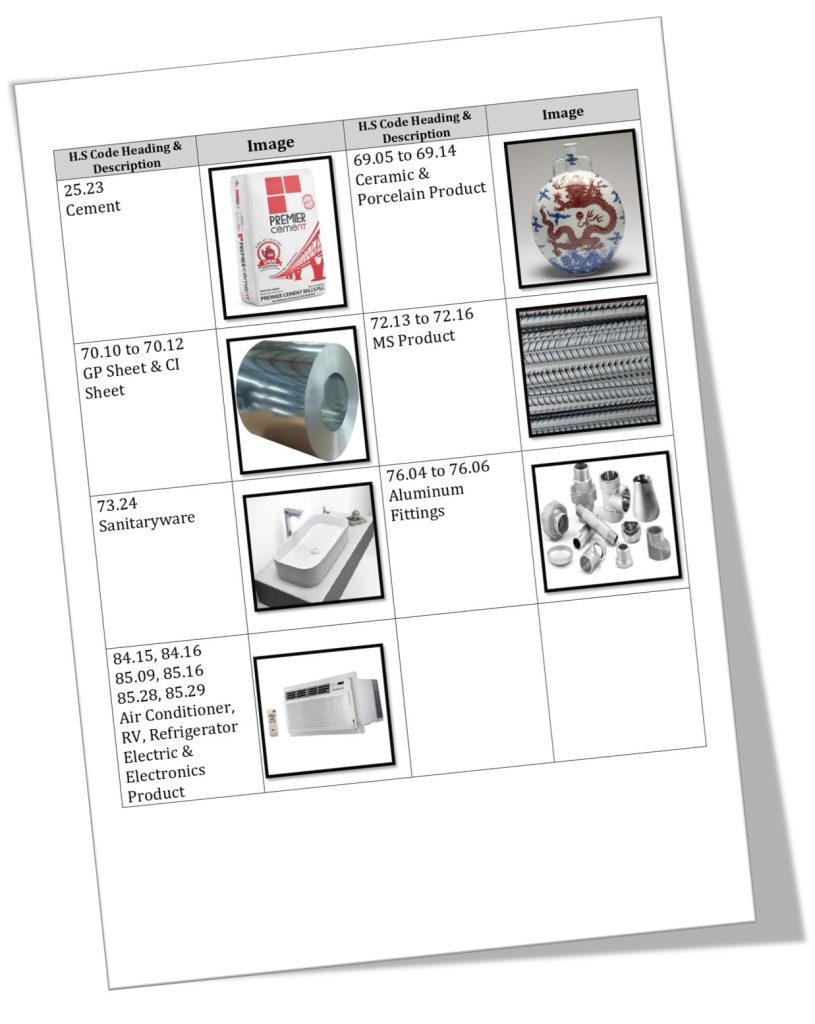

Additionally, as per General Order (GO) No.17/Mushak/2019—Date: 17-July-2019, mandatory VAT registration is applicable for those who manufacture goods, supply services and, goods as per Table 1,2 & 3 respectively of the said GO, irrespective of their turnover being below the VAT registration threshold.

Table-1 Manufacturer of goods

Chocolate, noodles, biscuit, soap, detergent, plastic goods, leather goods, wooden goods, all kinds of goods made of ceramic and porcelain, electric bulb.

Table-2 Service Provider

Construction firm, consultancy firm and supervisory firm, procurement provider, human resources supply or management organization, ITES etc.

Table 3 Trader

Cement, all kinds of goods made of ceramic and porcelain, GP Sheet/ CI Sheet, MS products, sanitary-ware, aluminum fittings, all kinds of electric and electronics goods including air conditioner, refrigerator, television.

►Super shop, shopping mall irrespective of place.

► Goods under table-3 in case of supply at trading stage by organization situated within the area of district town and city corporation.

In conclusion, unlocking the secrets of VAT registration & turnover enlistment in Bangladesh is vital for businesses operating in the country. we emerge not only with a clearer understanding but also with a newfound appreciation for its significance. VAT registration isn’t merely a bureaucratic formality; it’s a gateway to financial transparency, regulatory compliance, and business sustainability.